Raise Capital

Products

Resources

May 11, 2022

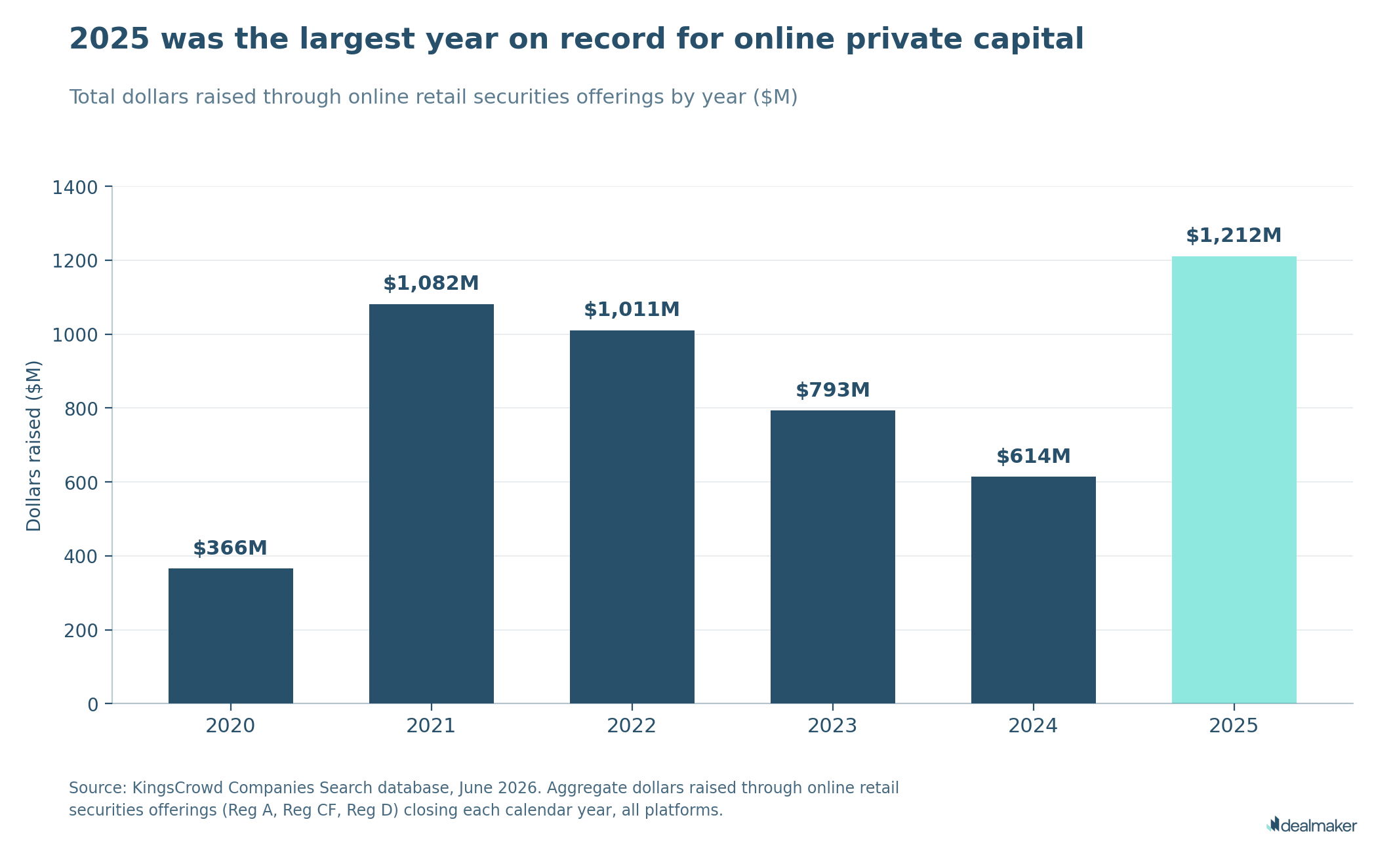

Regulation A ('Reg A' or 'Reg A+') is an SEC exemption that lets companies raise up to $75 million from the public, including non-accredited investors, without registering a full IPO. Reg A was long an obscure, rarely used section of the Securities Act of 1933. That changed in 2012, when the Obama administration signed the JOBS Act (Jumpstart Our Business Startups Act) into law. The JOBS Act directed the SEC to expand Regulation A, and the SEC's final rules, effective June 2015, created the current Tier 1/Tier 2 structure and gave rise to what's now called Reg A+, and equity crowdfunding as we know it today. With increased limits on how much a company can raise, the term 'mini-IPO' is now often used to describe capital raised by going direct to consumers as investors with equity.

Equity Crowdfunding is the process of raising funds for a company’s specific purpose (growth, expansion, launch, etc.) from the general public. What does that mean for companies looking for funding? With today’s technology and the internet allowing for a global reach, crowdfunding has become incredibly efficient: it now enables companies looking to raise capital to reach a much wider audience than traditional VC firms. Through equity crowdfunding, emerging companies can pitch their businesses directly to prospective investors, allowing an exciting business to raise needed capital to get off the ground.

As one law firm explains, both public or private companies in the US and Canada are eligible under Reg A+ to raise equity capital. But certain businesses are prevented from doing so:

Both public and private companies in the US and Canada are eligible under Reg A+ to raise equity capital. Reg A+ is commonly used by:

But certain businesses are prevented from using Reg A+:

Traditionally, companies that wanted to sell shares to the public (and raise capital that way) needed to register those securities with the Securities and Exchange Commission. Otherwise, they must rely on an exemption. Being able to rely on a prescribed exemption can be incredibly important for a company, as it means they're not subject to the same level of reporting requirements as registered firms. Indeed, in the case of Reg A+ offerings, the SEC notes: "...smaller companies in earlier stages of development may be able to use this rule to more cost-effectively raise money."

Beyond the cost savings, a Reg A+ offering can double as a marketing and branding tool. Running a raise publicly raises your company's profile and can attract new customers and partners alongside capital. And because Reg A+ allows you to "test the waters" before filing, it also gives you a read on market demand before you commit to an offering.

Companies pursuing a Reg A+ exemption from the SEC to raise capital must indicate whether they intend to sell shares under a Tier 1 or Tier 2 offering.

Tier 1 offering: Raise up to $20 million USD in any 12-month period. This figure may include up to $6 million USD in secondary sales by the issuer's affiliates.

Tier 2 offering: Raise up to $75 million USD from equity investors over the course of any 12-month period. This total may include secondary sales to a maximum of $22.5 million USD in secondary sales from their affiliates. That $75 million ceiling isn't where Reg A+ started. When the SEC first adopted the Tier 1/Tier 2 structure in 2015, Tier 2's cap was set at $50 million. The SEC raised it to $75 million in a rulemaking that took effect in 2021, one of several expansions that have made Reg A+ more useful to issuers since its creation.

EnergyX Raise Powered by DealMaker

Miso Robotics Raise Powered by DealMaker

A Reg A+ offering typically moves through these steps:

For a traditional, SEC-registered IPO, there is a strict prohibition (a "quiet period") on communicating with investors prior to the offering. Crucially, this communication ban is not imposed on Reg A issuers. Unlike their larger counterparts, Reg A+ companies are permitted to "test the waters" by communicating with prospective investors prior to the offering itself. This gives them a chance to gauge the public's interest in their equity securities. It is mandatory, though, to submit any promotional materials to the SEC along with the offering statement.

As mentioned, Reg A+ offerings are less onerous for companies than SEC registration. That said, there are still a number of requirements that prospective issuers must be aware of before selling shares to the public. For sales connected to Tier 1 offerings, a company must be compliant with all state-level qualification and blue-sky requirements. Blue-sky rules aim to protect the public from fraud via "the supervision and regulation of offers and sales of securities." Tier 2 saves the hassle of state-by-state registration. However, companies electing to rely on Tier 2 should note that they will be subject to ongoing reporting requirements after the offering has been completed, under Rule 257 of the Securities Act (annual, semi-annual, and current reports, detailed below), and that non-accredited investors in Tier 2 offerings are limited in how much they can invest.

Financial statement requirements also differ by tier: Tier 2 offerings require audited financial statements for the two most recently completed fiscal years. Tier 1 offerings are not required to be audited under federal rules, unless the company already had audited financials prepared for another purpose (state regulators reviewing a Tier 1 offering may have their own expectations).

Companies pursuing either a Tier 1 or Tier 2 offering must use Form 1-A to file an offering statement with the SEC. Included in this statement is the offering circular, which is the primary disclosure document provided to prospective investors. Issuers must either provide the circular to potential investors, or provide instructions for how it can be accessed. Before a company may actually sell shares to the public for money, its offering statement must be qualified by the staff of the SEC.

After completing a Regulation A+ offering, companies must continue to meet specific reporting obligations to maintain transparency and accountability:

Companies must also comply with investment limitations restricting how much non-accredited investors can invest in a Reg A+ offering. Maintaining an existing trading market for your securities is also important, since it lets investors buy and sell on a national securities exchange, providing liquidity and supporting investor confidence.

DealMaker is the leading platform for Reg A+ offerings, empowering founders and operators to raise capital efficiently and on their own terms. Our platform's hub of tools and services supports you throughout the entire Reg A+ process:

Regulation A+ empowers businesses to raise up to $75 million per year from their customers, followers, and fans, a transformative opportunity that can drive growth, increase brand awareness, and build real relationships between companies and their communities. Often called the "mini-IPO," Reg A+ offers a less intensive qualification process than a traditional IPO while still opening the door to the public markets. Talk to the DealMaker team about launching your own Reg A+ raise.

If it seems like a lot to remember, don’t worry. DealMaker makes it easy. With a raise through our platform, you can have peace-of-mind that you are meeting SEC requirements, filing the correct forms, and communicating to investors in a compliant manner.

Is Reg A+ the same as equity crowdfunding?

Not exactly, though the terms get used loosely. "Equity crowdfunding" most precisely refers to Regulation Crowdfunding (Reg CF), a separate JOBS Act exemption capped at $5 million per year. Reg A+ allows much larger raises, up to $75 million under Tier 2, with more disclosure requirements, closer to a scaled-down public offering than a crowdfunding campaign, even though both let everyday investors buy equity in private companies.

What's the difference between Reg A+ and Reg CF?

The biggest differences are raise size and process. Reg CF caps offerings at $5 million in a 12-month period and requires every transaction to go through an SEC-registered broker-dealer or funding portal. Reg A+ allows up to $20 million under Tier 1 or $75 million under Tier 2, with no broker-dealer or funding portal requirement, and Tier 2 issuers face additional obligations like audited financials and ongoing SEC reporting that Reg CF doesn't require. Read more about their differences here.

How long does a Reg A+ raise take?

There's no fixed timeline, but SEC staff research found a median of 78 days from initial filing to qualification. That covers SEC review only. Once qualified, most issuers then run their investor-facing raise for several additional months depending on their fundraising goals and marketing strategy.

Do I need a broker-dealer for Reg A+?

No. Regulation A+ has no broker-dealer or funding portal requirement in either tier, that requirement is specific to Regulation Crowdfunding. Reg A+ issuers can raise capital and sell securities directly through an online platform. Some issuers choose to bring in a broker-dealer for a Tier 2 raise anyway given the added complexity, but it isn't an SEC mandate.

What's required to qualify for a Reg A+ offering?

You need to submit business and financial information, a detailed use-of-capital breakdown, risk factors, management team information, and financial statements (audited for Tier 2, discussed below) for SEC review. Most companies work with securities counsel to prepare materials.

What are the financial disclosure requirements for Reg A+?

Requirements depend on your tier: Tier 2 offerings (up to $75M) must provide audited financial statements for the two most recently completed fiscal years. Tier 1 offerings (up to $20M) aren't required to be audited under federal rules unless the company already has audited financials for other purposes. Both tiers must disclose revenue, expenses, assets, liabilities, and cash flow. The financial statements also can't be stale: how recent they need to be depends on how much time has passed since your fiscal year end relative to when the offering is qualified.

Can companies raise from non-accredited investors under Reg A+?

Yes, that's the core advantage of Reg A+. Unlike Reg D (accredited investors only), Reg A+ allows anyone to invest, subject to investment limits. Non-accredited investors can typically invest up to 10% of their annual income or net worth, whichever is greater.

What happens after SEC qualification in a Reg A+ offering?

After qualification, you can launch your capital raise and begin accepting investor commitments. The offering typically closes in 30-90 days depending on demand. Companies can extend offerings or run multiple campaigns under the same qualification.

How do companies leverage Reg A+ for multiple raises and eventual public listing?

Reg A+ positions you for continuous capital raising. After your first qualification, you can launch additional offerings under the same qualification or file new ones as you grow. Since the SEC reporting you're doing mirrors public company requirements, an eventual IPO or exchange listing becomes significantly easier.

.png)

.jpg)

.png)