Raise Capital

Products

Resources

June 22, 2026

By Aaron Shafton, Managing Director at DealMaker Securities

Part 4 of 4 in the Private Capital Crisis series. Start with Part 1: IPOs are back, but not for everybody.

The numbers at a glance:

The capital exists. The access has been the missing piece, and that's changing faster than most Series B/C founders realize.

Part 3 walked through four pressures compounding on the 2021 cap table: liquidation preferences stacking, secondaries setting the real price, employee equity going underwater, and venture debt restructuring on top of all of it. All four trace back to the same problem: your existing investors are stuck on a 10-to-12-year fund clock you cannot move. The good news: there is a different clock available.

US retirement accounts hold $49.1 trillion in total assets, with $19.2 trillion in IRAs and $14.2 trillion in 401(k)s, according to the Investment Company Institute. That is roughly 96 times the entire 2025 global venture capital market, which totaled $512 billion in deal value, the second-highest annual total on record per PitchBook.

Last week, SpaceX priced the largest IPO on record, raising $75 billion at a $1.77 trillion valuation. SpaceX allocated roughly 20% of its shares to retail investors through broker-dealer channels, more than double the typical 5 to 10 percent retail share on an offering of this scale, CNBC reported on the day of pricing. The signal is clear: when the largest IPO ever recorded accommodates retail at twice the historical share, the institutional gatekeeping that used to wall off the biggest deals has cracked at the top of the market. It is cracking in the middle of the market too.

A growing share of US retirement and individual wealth is now legally and operationally accessible to private companies through the same securities frameworks that govern any other priced round. The question isn't whether retail capital is real. The question is why founders running into all four cap-table pressures are still treating it as a Plan C.

Retail capital is equity raised from individual investors rather than institutional ones, under one of three SEC frameworks. Same securities laws as any other priced round with audited financials, broker-dealer oversight, and regulated offering process. The investors are equity shareholders with the normal rights any shareholder has under Delaware corporate law. They are not "backers" and they are not crowdfunders.

Three SEC frameworks govern these offerings:

Regulation A, the mini-IPO. Up to $75 million per year from any individual investor, accredited or not. Requires audited financials and a qualified offering circular filed with the SEC. The framework for Series B/C scale. Read more about Reg A+ here.

Regulation CF, smaller equity crowdfunding. Up to $5 million per year, also open to any individual investor. Lower legal lift than Reg A. A common testing ground before a larger raise. Read more about Reg CF here.

Regulation D 506(c), accredited investors only. No raise cap, but participants must meet income or net-worth thresholds. Permits public marketing. Useful for larger checks from a narrower pool. Read more about Reg D here.

Most companies that scale retail use more than one over time, often starting with Reg CF before stepping up to Reg A.

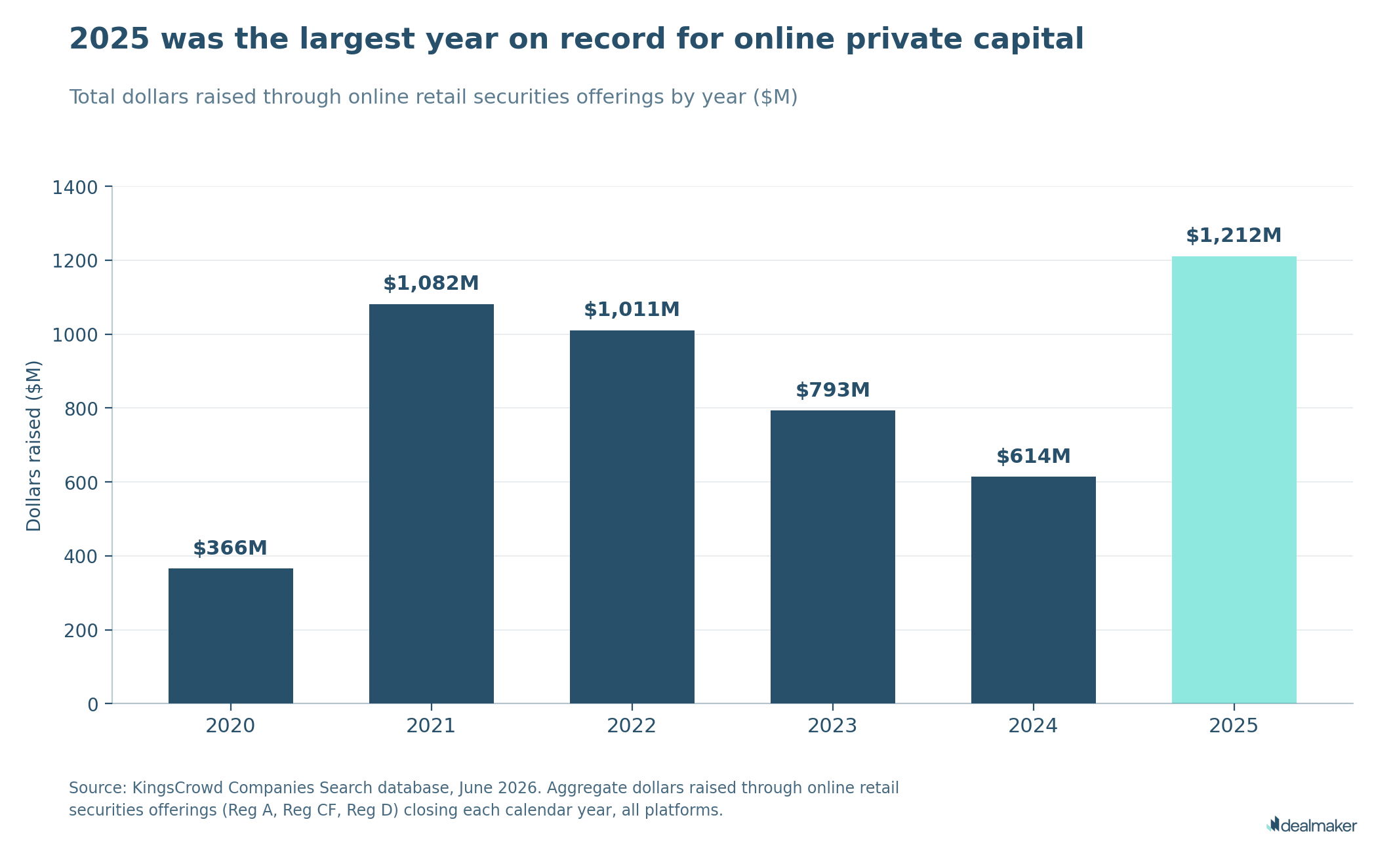

Online private capital markets have raised $6.27 billion across 9,295 funded companies all-time. In 2025 alone, 1,234 raises closed for $1.21 billion, per KingsCrowd. Roughly 3.1 million individual retail investors have participated across reporting companies, with a median of 90 investors per company and tens of thousands in the largest raises.

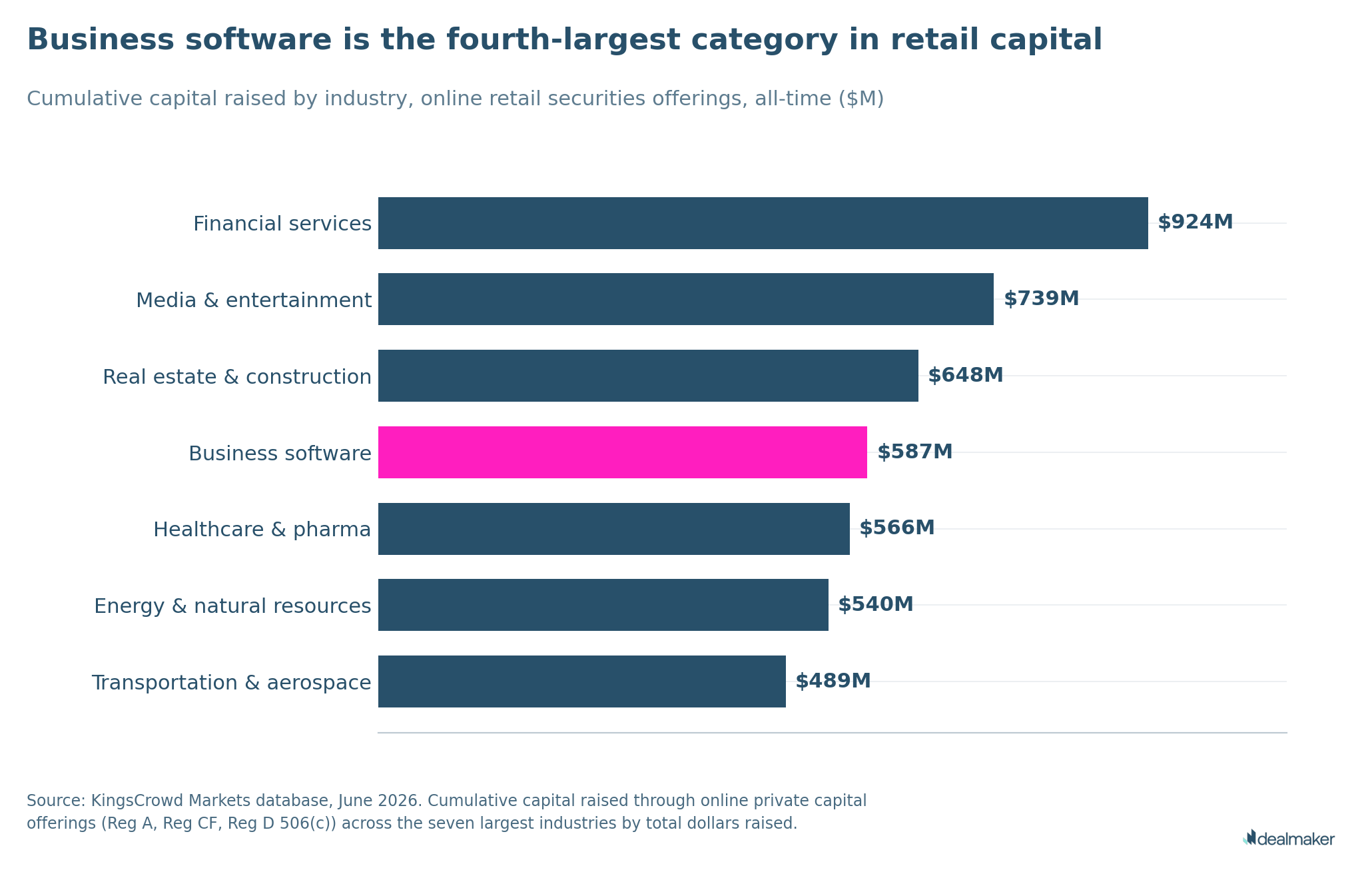

The industry mix is not what most founders assume. Business software is the fourth-largest category by cumulative capital raised. Healthcare, energy, transportation, and financial services round out the top tiers.

The asymmetry between addressable capital and addressable mechanism is hard to ignore. US retirement assets ($49.1 trillion) are roughly 96 times the entire 2025 global venture capital market ($512 billion). Online private capital raised through these frameworks all-time ($6.27 billion) is a fractional share of the addressable pool. The fraction is growing every year, and the structural shift in retail demand for private-market exposure is the reason.

Raise size at Series B/C scale routinely clears $50 million in Reg A. Recent examples include EnergyX (energy infrastructure, $75.5 million), RAD Intel (B2B AI marketing, $64.6 million), Newsmax (media, $64.1 million), Boxabl (modular housing, $63.6 million), and Pacaso (residential real estate, $60.6 million).

The timeline is six months or more from kickoff to close. A retail raise is an infrastructure build, not a flash event. The core requirements are audited financials, a legal structure that can absorb a broader shareholder base, investor relations and communications capacity, and a marketing engine that can qualify and convert at scale.

Managing a base of 500 to 5,000 retail shareholders carries running costs: investor communications, securities compliance, voting and consent mechanics. Real overhead, manageable in practice.

Every Series B/C founder reading this will silently object on:

"This is for B2C consumer brands." Not true. Business software is the fourth-largest industry in the online private capital market ($587 million cumulative, per KingsCrowd). Healthcare, energy, and transportation round out the top tiers. The companies that have run substantial retail raises include EnergyX (B2B cleantech infrastructure, $75.5 million), RAD Intel (B2B AI marketing software, $64.6 million), and Newsmax (media, $64.1 million). The fit is about narrative accessibility, not consumer-versus-B2B taxonomy.

"It signals weakness to institutional investors I'll need later." The institutional view has shifted. Retail demand is increasingly read as proof of customer or audience traction, not as a substitute for institutional credibility. EnergyX's founder has described retail as the round that de-risked the company for institutional follow-on by GM, Posco Holdings, and the US Department of Energy. Pacaso raised $200 million from traditional venture capital alongside $60.6 million from retail investors. The two channels coexist. And when the largest IPO in history (SpaceX, $75 billion, June 11, 2026) allocates roughly twice the typical retail share to individual investors, the argument that retail demand signals institutional weakness no longer holds at any altitude of the market.

"I don't have time to run a marketing campaign for retail." You don't have time not to. The alternative is the brutal down round we covered in Part 3, including the participating preferences, the underwater employee equity, and the venture debt restructuring that compounds on top. The retail infrastructure exists, the operational lifting is well-mapped, and the timeline (six months from kickoff) is exactly the runway most Series B/C companies have left before the next round becomes urgent.

The comparison isn't retail capital versus venture debt or an institutional round. It is retail capital versus what happens to your cap table without any liquidity mechanism in place.

A 30% down round costs more than 30%. It damages founder ownership, employee morale, recruiting, and customer perception simultaneously, and it costs you the next year of execution while you re-stabilize the company. Retail capital, well-run, lets you sidestep that scenario: a different pool of investors, different terms, a different timeline.

Build the liquidity mechanism yourself, before you need it.

If your last priced round was 2020, 2021, or 2022, here is the action list.

The founders who will look good in three years are the ones who priced this risk honestly and built the mechanism to manage it before they needed to.

We publish quarterly private capital data most Series B/C founders don't see. Subscribe to get the Q2 numbers the week they drop.

Aaron Shafton is a Registered Representative of DealMaker Securities LLC ("DMS"). The views and opinions expressed in this article are solely his own and do not represent the views, positions, or opinions of DMS or any of its affiliates. This article is for informational purposes only and does not constitute investment advice, a solicitation, or an offer to buy or sell any securities. The data and analysis presented reflect publicly available sources as of the date of publication and are subject to change. Nothing in this article should be relied upon as the basis for any investment decision. Readers should consult a qualified financial advisor before making any investment.

.png)

.jpg)

.png)