Raise Capital

Products

Resources

June 4, 2026

By Aaron Shafton, Managing Director at DealMaker Securities

On the secondary market, 82% of unicorns trade below their last priced round, and 22 of them trade at discounts of more than 20%. If your Series B or C closed in 2020, 2021, or 2022, the secondary market is already pricing your equity in 2026, and the price is different from the one on your last term sheet.

Secondaries are one of four signals telling you that your 2021 round is still working against you. Liquidation preferences are stacking against founders and employees. Employee equity is going underwater. Venture debt taken in 2022 and 2023 is restructuring on cap tables across the cohort. Most founders model these in isolation, when in reality they compound. This is the cap-table problem that doesn't show up cleanly in any single quarterly report.

Start with the LPs: vintage 2021 venture funds are four years into a 10-to-12-year clock, and the math behind that clock is unforgiving.

CalSTRS, the second-largest US public pension fund, manages $367.7 billion across roughly one million current and retired California educators. About 15% of that, $55 billion, sits in private equity. Across its 2021 vintage venture commitments, the capital that has actually come back to the fund is roughly 3% of what was invested. The portfolio is marked at about $1.18 for every $1 invested, on paper. That's normal for a four-year-old venture fund and entirely consistent with how the J-curve is supposed to work. It's also the structural reason your existing investors have gotten quieter about leading your next round than they were two years ago.

The bigger pressure sits on smaller LPs. Family offices, individual high-net-worth investors, and smaller fund-of-funds have less patience than a teacher pension fund and louder voices on Series B/C cap tables. Same expectations on getting capital back, different temperament.

This is a cohort dynamic, not a critique of any individual venture firm. Most 2021 vintage funds are doing exactly what their partnership agreements allow them to do. The upstream context still matters. The next four sections are what's already showing up on your cap table because of it.

Liquidation preferences are stacking. When you raised your Series C in 2021, the standard term was clean: 1x non-participating preferred, no senior preference, no pay-to-play. In a sale, your investors got their original investment back first, then the remaining proceeds split among everyone, including founder common stock, on an as-converted basis. Founders and employees still saw real upside in any reasonable exit.

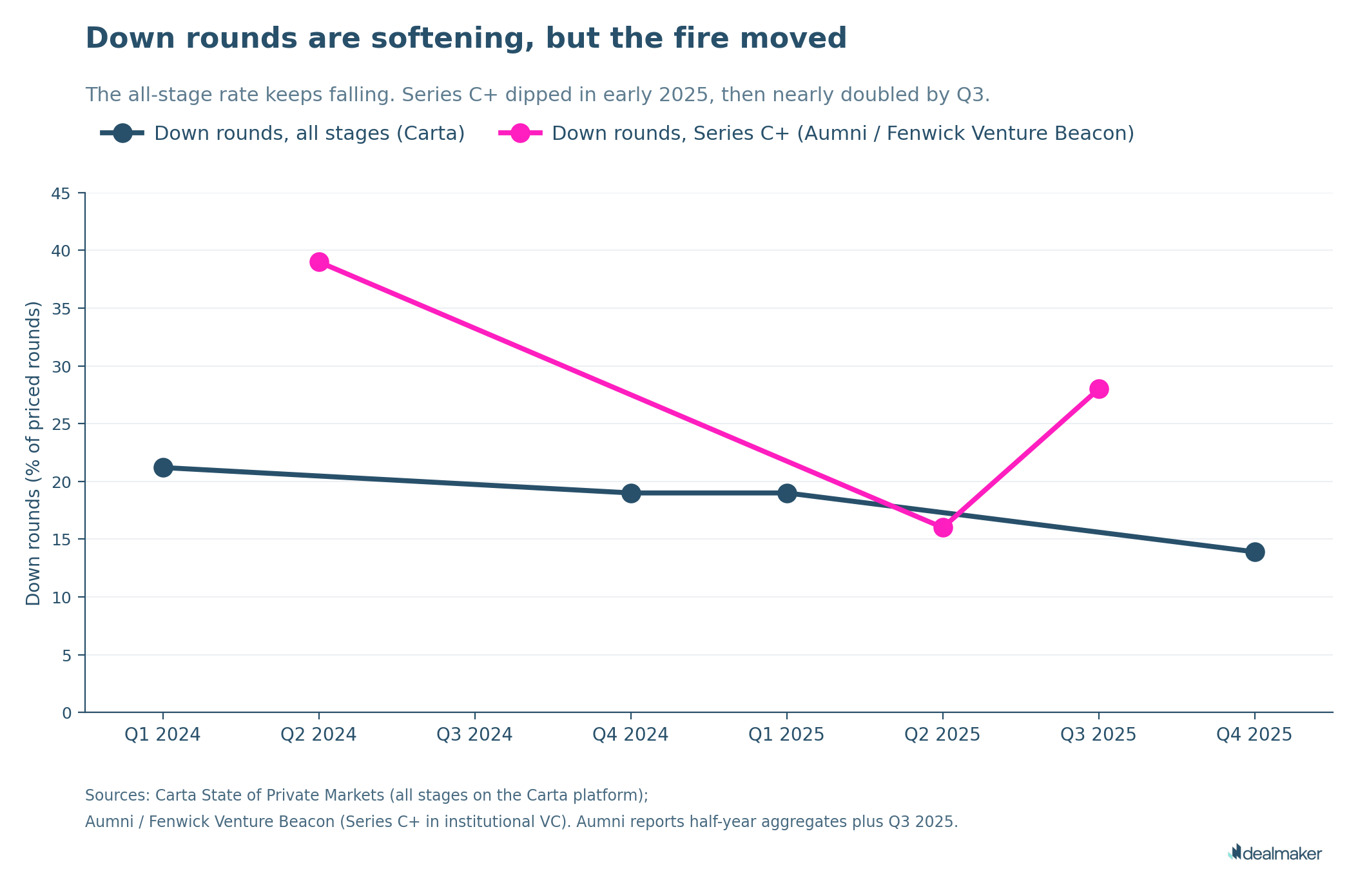

The 2026 term sheet looks different. Down rounds among Series C and later companies nearly doubled from 16% in the first half of 2025 to more than 28% by the third quarter, according to the Aumni and Fenwick Venture Beacon. Pay-to-play clauses, which force existing investors to participate in the new round or lose part of their preferred stock, hit 10.1% of new rounds in early 2026, the highest rate since 2014. Redemption rights, which let investors demand their money back at a fixed future date, jumped from 1.8% to 6.1% in a single quarter, Cooley reports.

A new investor coming in at a flat or down valuation in 2026 will negotiate harder than your original lead did. They'll want a participating preference, which means they take their money back first and then also share in the remaining proceeds. They'll want a multiple, maybe 1.5x or 2x their investment paid back before anyone else. And they'll want to sit senior to your existing 2021 investors in the payout order, meaning the new round gets paid in full before any 2021 preferences get a dollar. Each new layer pushes founder common stock further behind in any exit scenario.

Affinity offers a useful illustration of the math: the company raised $80 million in Series C funding at roughly a $600 million post-money valuation in 2021. Imagine a hypothetical 2026 Series D of another $80 million at the same valuation, with a 1.5x participating preference and senior position in the stack. In a sale, the new investors collect $120 million off the top before anyone else sees a dollar. The original Series C investors then collect their $80 million. Founder common stock, plus any employees who exercised options, splits whatever remains. Below a $200 million sale price, founders and employees walk away with nothing.

Secondaries are setting the real price. The secondary market is the other half of the repricing. Buyers and sellers are already trading shares in private companies at prices that contradict last-round valuations. According to Caplight, 82% of unicorns trade below their last primary round, with 22 names sitting more than 20% below. Sub-decacorn private companies, which is most of the Series B/C cohort, trade at average bid discounts of roughly 39% to last round, Hiive reports.

Even LP positions in venture funds are repricing. Fund interests are clearing the secondary market at roughly 75% of net asset value, according to Setter Capital's H1 2025 volume report. LPs taking a 25% haircut just to exit fund positions tell you what your equity is worth to anyone trying to price it today.

If your last round was a 2021 Series C at $600 million and you're modeling a follow-on at the same valuation or higher, the secondary market has already given you a different number to work from.

Cap tables are a finance problem until they become a retention problem, and by the time retention is the problem you're solving, the people who could have helped you fix it are already updating their LinkedIn.

That's why employee equity has to be modeled inside the cap-table picture, not next to it. The data here is sharp. In the fourth quarter of 2024, employees at private companies exercised only 32.2% of their vested, in-the-money options, according to Carta. Three years earlier the same number was 54.2%. The drop isn't subtle.

The reason is mechanical: exercising an option costs money. The employee pays the strike price, and depending on the option type and the spread between strike and current fair market value, often pays tax on the difference. If the secondary market is pricing the company below the strike-plus-tax math, exercising is a losing trade for the employee. They wait, hoping for an exit, or they leave.

Tender offers, which let employees sell vested shares back to the company or to a new investor, grew 62% year over year in 2025, reaching 396 deals and $18.4 billion in total volume, Carta also reports. That headline number disguises what's really happening. Tender activity is concentrated in the same top-decile names that dominated the funding chart in Part 2. Anthropic recently held a tender that came in short of its $6 billion target because employees refused to sell, expecting more upside. Companies outside that top decile aren't getting tender offers at all.

Liquidity is a people problem before it's a finance problem.

This is distinct from the bridge round mechanics covered in Part 2. Bridge rounds extend equity runway. Venture debt is a loan, which means in a sale or restructuring, the lender gets paid in full before any equity holder, including the most senior preferred shareholders, sees a dollar.

Venture debt issuance hit a record $53.3 billion in 2024, up 94.5% year over year, even as the total number of venture deals fell to a decade low, according to a joint Runway Growth and PitchBook review. Money concentrated in fewer companies and bigger checks. A lot of that capital flowed to Series B/C companies in 2022 and 2023 because equity rounds were harder to close and the math on a $20-to-$40 million term loan looked manageable at the time.

The terms on those loans are now becoming a cap-table event. Covenants are tighter than founders remember, and most venture debt comes with warrants, which give the lender the right to buy equity at a preset price. Warrants typically activate or accelerate on default or restructuring. When the debt restructures, the warrant exercise sits on top of the existing liquidation preference stack as another layer of dilution.

Runway Growth Finance, a publicly traded venture debt lender, reported that its net asset value per share dropped 9.6% in a single quarter, from $13.42 to $12.13, in Q1 2026. Two of its portfolio companies, Marley Spoon and Blueshift, moved to non-accrual status, meaning the lender no longer expects to be paid in full on those loans.

Blueshift raised a $30 million Series C in February 2021, led by Fort Ross Ventures and Avatar Growth Capital, with about $65 million in total equity raised over its lifetime, TechCrunch reported. In January 2024, the company took a $40 million growth investment from Runway Growth, refinancing existing debt and funding expansion. Two years later, that loan moved to non-accrual. The restructuring is ongoing and the founder remains in place, but the cap table that started as a clean 2021 Series C is now a different document entirely.

The loan that bought you 18 months of runway in 2023 is rewriting your cap table in 2026.

The headline number looks reassuring. Down rounds across all stages dropped from 21.2% in the first quarter of 2024 to 13.9% in the fourth quarter of 2025, as Part 2 established.

The instinct is to read this as recovery. The mechanism says otherwise. Down rounds are falling because the most distressed companies aren't pricing rounds at all. They're bridging, restructuring, or shutting down. The companies that survive to a priced round are a healthier subset by definition, which means survivorship bias is making the data look better than the underlying cohort.

The pressure didn't disappear, it moved. Into the space between rounds, where bridge structures and extension financings absorb the shock. Into the secondary market, where prices set the real valuation. Into the cap table itself, through stacked preferences, venture debt warrants, and underwater employee equity.

A cap table that looks fine is not the same as a cap table that is fine. Without a priced round to force the math into the open, pressure migrates into preferences that stack quietly, debt that restructures quietly, and employee equity that goes underwater quietly. The fire is invisible because no one is lighting a match. By the time the drift stops looking like drift, it has already done the damage.

If your last priced round was 2020 to 2022 and the math above looks familiar, you have three options that actually exist in the current market.

The first is to reset on harder terms. Accept a down round or an extension with participating preferences, multiples, or pay-to-play provisions. This is the most painful upfront and the cleanest in the long run. You stop pretending the 2021 valuation is the right number, you reprice cleanly, and you preserve optionality for the next four years.

The second is to cut to default-alive and wait. Reduce burn to near zero, extend the runway long enough to outlast the cycle, and trade growth for survival. Some categories support this. Most do not, and many companies that take this path quietly become something other than a venture-scale business in the process.

The third is to build the liquidity mechanism yourself. Open the cap table to capital that isn't waiting on the same return clock as your existing investors. Retail investors, accredited individuals, and family offices investing alongside priced rounds operate on different timelines and different expectations. This is the path that breaks the assumption that your investor base has to be the same investor base you started with.

Most founders model option one as the worst case and option three as exotic. The cap-table math from the four pressures above suggests option three is increasingly the only path that doesn't compound the existing pressure.

Your 2021 round didn't fail, but it's still alive, still on your cap table, still earning preferences for its holders every quarter you go without an exit or a follow-on. The four pressures in this post compound on each other in ways that don't show up cleanly in any of your existing models.

The good news is there's a $49 trillion source of capital that operates on a different clock entirely.

→ Read Part 4: Retail capital is a $49 trillion asset class you're treating as Plan C

Aaron Shafton is a Registered Representative of DealMaker Securities LLC ("DMS"). The views and opinions expressed in this article are solely his own and do not represent the views, positions, or opinions of DMS or any of its affiliates. This article is for informational purposes only and does not constitute investment advice, a solicitation, or an offer to buy or sell any securities. The data and analysis presented reflect publicly available sources as of the date of publication and are subject to change. Nothing in this article should be relied upon as the basis for any investment decision. Readers should consult a qualified financial advisor before making any investment.

.png)

.jpg)

.png)

.jpg)