Raise Capital

Products

Resources

May 21, 2026

By Aaron Shafton, Managing Director at DealMaker Securities

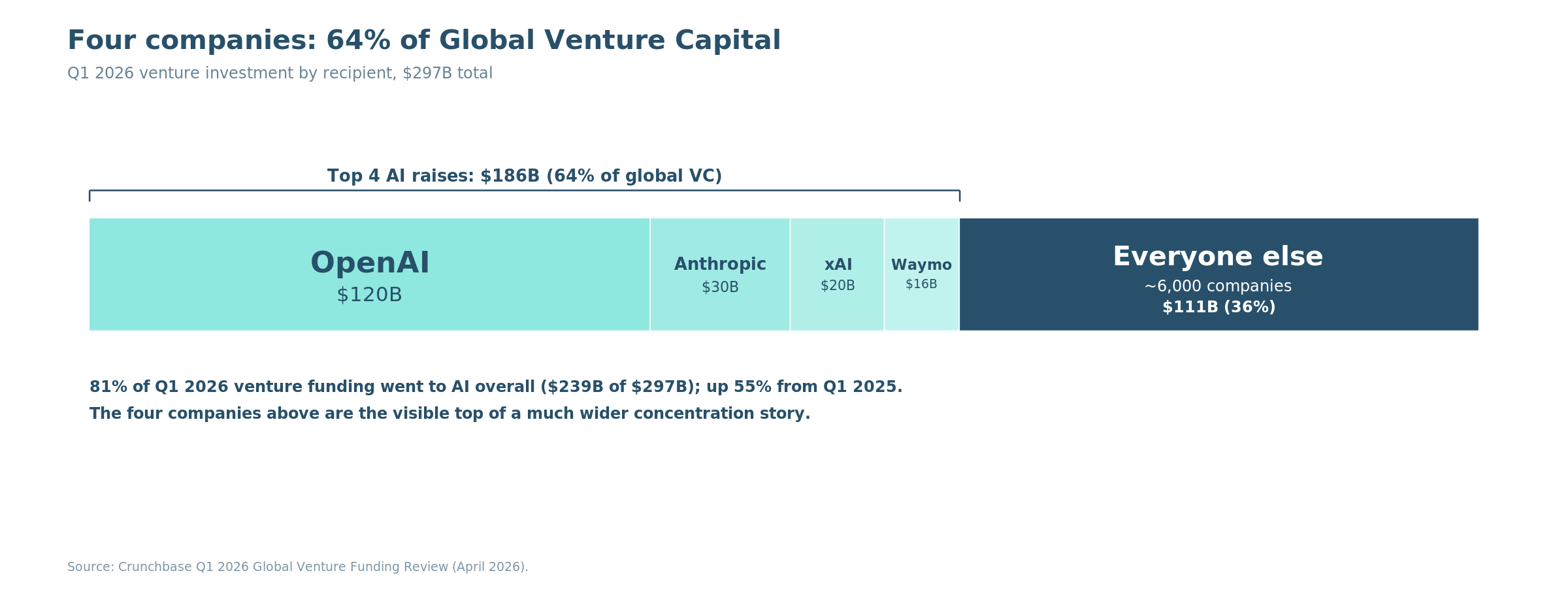

In Q1 2026, OpenAI raised $120 billion in a single financing round (Crunchbase). That's more than every Series A round on the entire Carta platform raised together for all of 2025 (Carta).

OpenAI wasn't alone. Anthropic raised $30 billion. xAI raised $20 billion. Waymo raised $16 billion. Together those four companies absorbed $186 billion, or 64% of the $297 billion in total global venture investment that quarter. AI startups overall captured 81% of all new venture funding globally, up from 55% just one year earlier. Total Q1 2026 venture investment alone equaled roughly 70% of all 2025 venture spending.

If you're a Series B or C founder outside the AI category, your fundraising experience and the headline funding totals are telling you opposite stories. The same dynamic that clipped Figma 85% from peak in nine months is the dynamic absorbing 81% of the new dollars. Capital flowing to AI is capital not flowing to you.

The IPO penciled into your Series D deck is the least reliable variable in your future. The Series C you raise to get there is the second-least reliable. Series B/C founders who haven't honestly priced both risks are carrying both anyway.

In November 2024, Bowery Farming told employees it was ceasing operations. The marquee U.S. vertical farming company had raised more than $700 million from First Round Capital, General Catalyst, and GV, plus $150 million in debt from KKR (TechCrunch). Its peak valuation was $2.3 billion with celebrity backers including Natalie Portman and Justin Timberlake. The company spent months trying to find a buyer, but couldn't. 187 workers were laid off across Pennsylvania and Maryland and the lights dimmed on a $2.3 billion private company because it could not bridge to the next round.

Bowery is not an outlier. SimpleClosure's 2025 State of Startup Shutdowns report found that Series A shutdowns jumped from roughly 6% to 14% of all closures in 2025, a 2.5x year-over-year increase (SimpleClosure). Series A failures in 2025 averaged seven years old. They were founded between 2017 and 2019, the era of fintech, proptech, logistics, HR tech, and B2B SaaS. These are companies that raised institutional capital, built real product, hired teams, generated real revenue, and still could not make the next round work.

SimpleClosure CEO Dori Yona puts it directly: "The correction has moved from 'failed ideas' to 'failed models.'"

The same SimpleClosure data shows the squeeze hitting multiple non-AI categories at once. B2B SaaS shutdowns rose from 5.2% to 7.7% of total closures. Climate and energy from 2.0% to 2.8%. Healthcare from 0.8% to 2.8%.

Bowery Farming’s collapse fits a broader pattern: 60% of all global venture capital and 70% of US venture capital went to $100M+ megarounds in 2025, a record high, with the lion's share of those checks going to AI (Crunchbase, October 2025). Crunchbase's framing is direct: early-stage funding has "essentially flatlined," and biotech investment as a share of overall funding hit a 20-year low. The total dollars went up, and the number of companies receiving them went down.

If your company is at Series B or C today, having raised in the 2020 to 2022 vintage, you are in the cohort the data shows is hitting the wall hardest.

At seed, AI and non-AI start basically even. The gap opens at Series A (84%) and reaches 3.7x by Series E+. It widens at every stage (PitchBook-NVCA). Carta's full-year 2025 review confirms the pattern from a different dataset: median AI premium at Series A is +38%, and at Series E+ it reaches +193%.

The fund-side dynamic explains why this compounds. In Q1 2026, six firms (Andreessen Horowitz, Thrive Capital, Founders Fund, Battery Ventures, Kleiner Perkins, and Lux Capital) raised $36.4 billion across the quarter, or 76% of all U.S. VC commitments. The other 166 funds that raised in Q1 split less than a quarter of new capital between them. Those mega-funds have to deploy at scale, and the only deals scaled to absorb $1B+ checks are the same handful of AI mega-rounds. LPs concentrate into mega-funds. Mega-funds concentrate into mega-AI deals.

The bifurcation runs all the way up to LPs themselves. Sophisticated allocators with established manager relationships and dedicated co-investment teams can underwrite an AI deal inside the category's 1.3-year round cadence. Their under-resourced peers can't, and they're getting locked out of the deals that are driving fund returns. PitchBook senior VC research analyst Kaidi Gao put it directly in a recent research note: "LPs that want in now are probably late to the party." The closed loop isn't just hard for non-AI founders to break into. It's hard for new LP money to break into too.

Net distributions to LPs have been negative since 2022, which means the capital is recycling inside that closed loop without fresh outside money pulling it in different directions. The cycle reinforces itself.

For a non-AI Series B/C founder, that's what the math actually looks like in practice. The round size you'd raise at the median is roughly 60% smaller than the AI peer in your investor's deck. You'll wait roughly six months longer between rounds. And the firms with the most capacity to write meaningful checks aren't focused on your category.

The cost of being outside the AI category isn't just smaller round sizes. It's longer time between rounds, more dilution per dollar raised, and more dependency on bridge financing.

Carta's 2025 data tells the story:

Bridge rounds have roughly doubled across every stage. At Series E+, they jumped from a 10% historical norm to 20% in 2025: one in five financings is now a bridge instead of a new round. 16.6% of all cash raised in Q2 2025 came via bridge rounds, up from 11.8% the year prior (Carta Bridge Rounds). $7.1 billion in bridge funding was deployed in H1 2025 alone.

The mechanical reason underneath the bridge-round surge matters. VC return models assume portfolio companies hit milestones inside the fund's investment window. When the median company can't, capital reroutes to the bets that can match the timeline and chase a power-law outcome. In 2026, that means AI. Bridge rounds keep your company alive while the fresh capital flows to a different category.

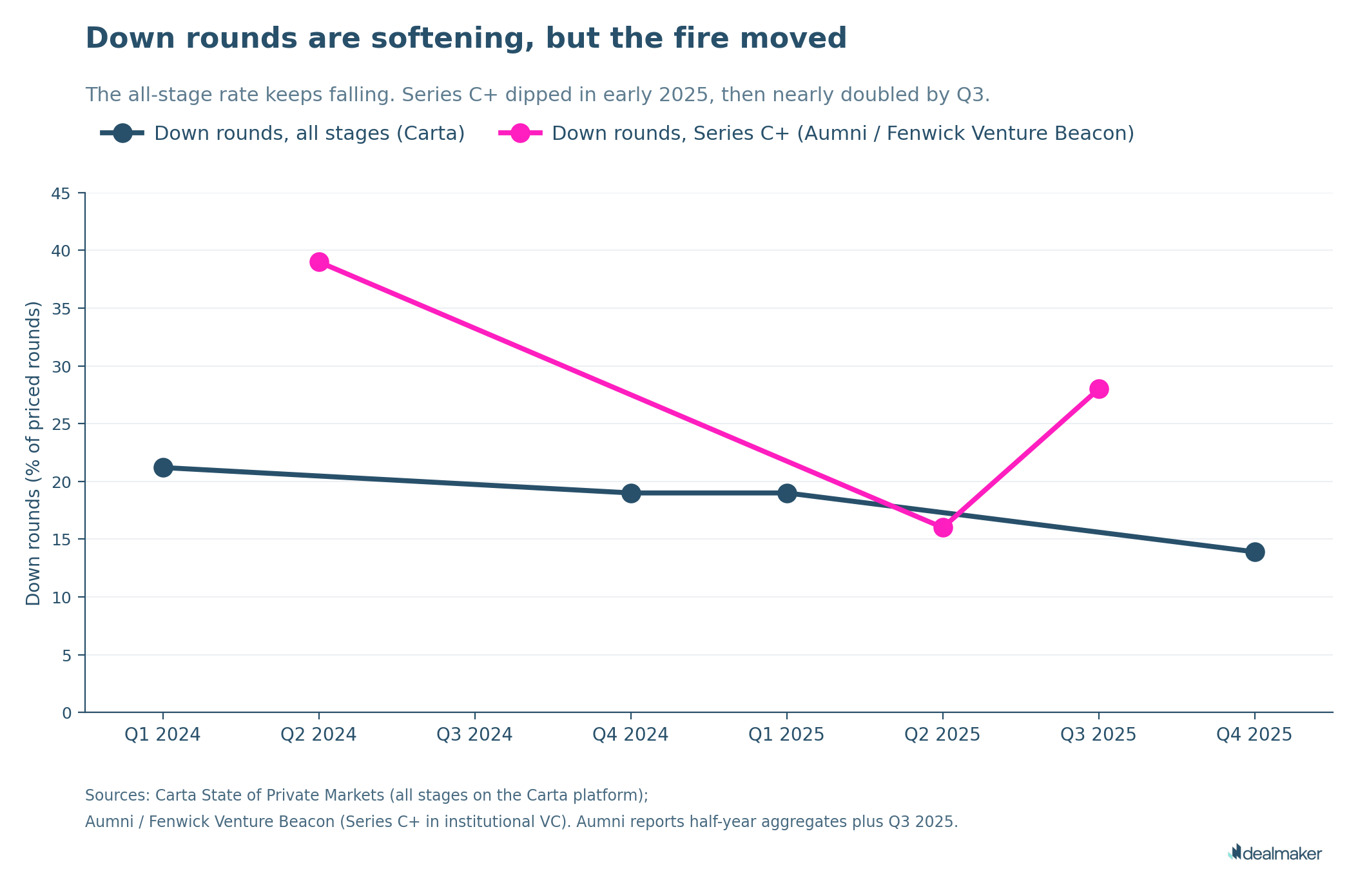

Down rounds in Q4 2025 hit 13.9%, recovering from a 21.2% peak in Q1 2024 but still well above the pre-ZIRP norm of 9 to 10%.

Bowery is the version of this where the bridge wasn't enough. Most of the 2017-2019 cohort SimpleClosure flagged didn't fail at the idea stage. They failed at the model stage, after they'd already raised the rounds Series B/C founders are raising right now.

This is the cost of being a non-AI Series B/C founder in 2026 even before you account for the IPO question.

Even the optimistic 2026 scenario hurts you. PitchBook flagged it in its Q1 monitor: if SpaceX, OpenAI, or Anthropic file (each potentially the largest IPO in history), they could "absorb available underwriting capacity and institutional allocation," pushing the broader IPO return into 2027. The mega-IPO scenario you've been hoping for is the same scenario that pushes your IPO out another year, against a venture market that's already been priced against you for at least four.

Three concrete operational decisions follow from this.

Stop modeling the next round on the last one. The Series C you raise in 2026 isn't going to look like the Series C your 2021 peer raised. Model around the same valuation or lower, stricter terms, longer wait, even if your metrics improve.

Track non-AI peer valuations in your category, not the AI-adjacent companies your VC will compare you to. Your investors will reach for AI peers because that's where the deal flow is. Push back with the right comparable set: companies in your stage and category that are non-AI. They are the right benchmark for your business and the wrong one for your VC's narrative.

Treat alternative capital as primary, not backup. Bridge rounds, structured rounds, secondaries, and retail capital are where the next 18 months of liquidity will actually come from for most non-AI Series B/C founders. They aren't a Plan B. They're a plan that keeps you alive and lets you keep control of the company.

Stanford lecturer Steve Blank, who teaches the school's Lean LaunchPad startup class, put the broader dynamic plainly in a recent Atlantic profile of Silicon Valley's young-founder economy: "If you have no core beliefs, then you follow the money; you follow what's most exciting" (The Atlantic). Your investors are following the money. The money is following AI. That's the operating environment you're building in, whether your category is AI or not.

Liquidity has to be engineered. Engineering takes time.

If the next round is unreliable, the next obvious question is what's already on your cap table.

It compounds.

The 2021 vintage round you closed at peak valuation isn't dead. It's still working against you. The 2026 cap table is where the macro pressure becomes operational, and most founders haven't priced that risk either.

→ Read Part 3: The cap table timebomb you're not pricing in

Aaron Shafton is a Registered Representative of DealMaker Securities LLC ("DMS"). The views and opinions expressed in this article are solely his own and do not represent the views, positions, or opinions of DMS or any of its affiliates. This article is for informational purposes only and does not constitute investment advice, a solicitation, or an offer to buy or sell any securities. The data and analysis presented reflect publicly available sources as of the date of publication and are subject to change. Nothing in this article should be relied upon as the basis for any investment decision. Readers should consult a qualified financial advisor before making any investment.

.png)

.jpg)

.png)

.jpg)

.jpg)