Raise Capital

Products

Resources

December 30, 2025

Going public doesn't have to mean choosing between institutional investors and your community. Today's most successful companies are doing both.

The journey from private to public doesn't have to follow the traditional playbook anymore. Regulation A combined with strategic planning creates a proven route to major exchange listing.

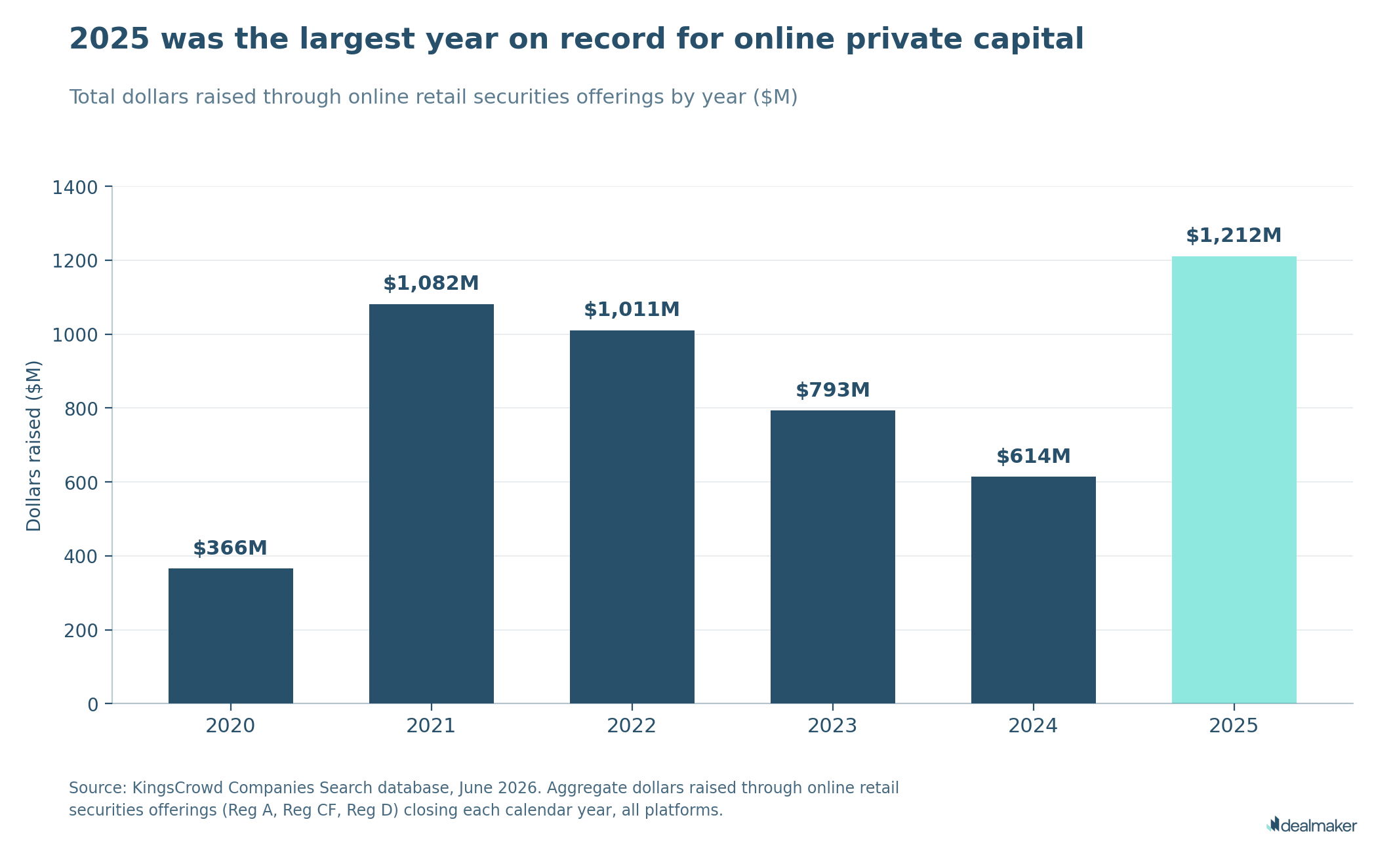

This isn't just theory. Multiple companies have successfully used Reg A to build investor communities of 5,000-40,000 shareholders, validate their markets, and position themselves for exchange listing. The result: permanent shareholder bases that fuel growth long after the initial raise closes.

Here's the reality: founders and executives need to understand the complete path from Reg A to public markets, including financial requirements, governance standards, operational infrastructure, execution strategies, and key performance indicators that determine success. This comprehensive guide walks you through everything you need to know about moving from a Regulation A offering to major exchange listing.

Disclaimer: This guide is educational only and not legal or financial advice. Consult securities counsel before pursuing any capital raising strategy.

Regulation A, commonly called Reg A, is a provision of the Jumpstart Our Business Startups (JOBS) Act that allows companies to raise capital directly from the public without traditional venture capital intermediaries. Unlike private placements that restrict investors to accredited individuals, Reg A offerings allow both accredited and non-accredited investors to participate.

Regulation A has fundamentally changed how companies approach capital raising. Instead of relying solely on institutional investors and venture capital firms, companies can now build communities of retail investors who become long-term shareholders and brand advocates.

Regulation A offerings come in two tiers, each with different capital raising limits and regulatory requirements:

Regulation A Tier 1 Offerings

Regulation A Tier 2 Offerings

Both Tier 1 and Tier 2 Regulation A offerings require companies to file a Form 1-A with the SEC, undergo SEC qualification, and maintain continuous disclosure obligations to shareholders. This regulatory foundation is critical because it prepares companies for the reporting and governance requirements that NASDAQ demands.

Regulation A serves as a bridge between private capital raising and public market listing. Companies that use Regulation A are essentially running a "public company dress rehearsal" before their official NASDAQ listing.

During a Regulation A raise, companies must:

This preparation work directly translates to NASDAQ listing readiness. The operational discipline, financial reporting rigor, and investor management systems built during Regulation A become the foundation for your public market operations.

Regulation A has emerged as a strategic stepping stone to NASDAQ listing for several compelling reasons. First, Regulation A requires audited financial statements prepared according to PCAOB standards, which are the same standards required for public companies. Second, Regulation A demands continuous disclosure obligations that mirror public company requirements. Third, Regulation A allows companies to build substantial shareholder bases before exchange listing.

Companies that use Regulation A are building the operational infrastructure and financial reporting discipline that NASDAQ demands. You're not starting from zero when you apply for NASDAQ listing. You're starting with proven operational systems, experienced management teams, and established shareholder bases.

The regulatory foundation matters tremendously. Companies that have successfully completed a Regulation A raise have already demonstrated:

Your Regulation A raise builds a retail-heavy shareholder base. Many founders worry this will hurt their exchange listing chances. The opposite is true. Those retail investors don't disappear when you uplist. Instead, they become your core holders, your brand ambassadors, and proof of market demand to institutional investors.

Pacaso CEO Austin Allison noted that exploring Regulation A+ forced deeper thinking about their business: "It was something that kind of stumbled across our desk somehow. But as we dug deeper into the opportunity, we became so bullish on this as a channel that it seemed obvious to us that this is how we wanted to raise our fourth round of capital."

This deeper analysis—understanding your market, your mission alignment, your investor base—is exactly the discipline that exchange listing requires.

The transition from Regulation A issuer to exchange-listed company requires discipline across multiple dimensions:

1. Investor Base Maturity and Evolution

During Regulation A, your messaging is acquisition-focused: "Join our community. Become a shareholder. Support our mission." Post-NASDAQ, your messaging becomes retention-focused: "Hold your shares. Participate in our growth. Benefit from our success."

Your Regulation A investors need to understand that listing represents a milestone, not an exit opportunity. Companies that successfully retain their Regulation A shareholders post-listing see:

2. Governance Upgrade: Building Exchange-Grade Governance

Regulation A requires basic governance structures. NASDAQ requires significantly more rigorous governance standards. You'll need to implement:

3. Reporting Rigor: Shifting from Annual to Quarterly Disclosure

During Regulation A, you file annual Form 1-A updates. As a NASDAQ company, you file quarterly 10-Q reports, annual 10-K reports, and current 8-K reports for material events. This represents a significant increase in reporting frequency and complexity.

4. Market Maker Relationships: Building Liquidity Infrastructure

Before NASDAQ listing, you need to cultivate relationships with 3-4 market makers who will commit to making a market in your stock. These relationships are critical because market makers provide liquidity, which attracts institutional investors.

Most companies follow a predictable pathway from Regulation A to NASDAQ listing. Understanding this pathway helps you plan your timeline and prepare appropriately.

The Standard Reg A to NASDAQ Pathway

Phase 1: Regulation A Qualification (Months 0-6)

Phase 2: Operational Preparation (Months 6-12)

Phase 3: NASDAQ Application (Months 12-18)

Phase 4: NASDAQ Review and Approval (Months 18-24)

Total Timeline: 18-24 Months from Regulation A Qualification to NASDAQ Listing

Many founders believe that institutional investors will avoid companies with large retail shareholder bases. Research shows the opposite. Institutional investors actually prefer companies with:

Exchange visibility improves analyst coverage. Analyst coverage drives institutional investor interest. Your retail investor base provides:

Before your NASDAQ application lands, you need to meet quantitative and qualitative thresholds. The Nasdaq Stock Market is a national securities exchange regulated by the SEC, with Nasdaq Stock Market LLC serving as the regulatory and listing entity responsible for enforcing and proposing listing standards for public companies. These requirements determine whether you’re eligible to list and what happens after listing begins.

All companies seeking to list on the Nasdaq stock market must comply with SEC laws and file a registration statement. A company is not required to retain a compliance adviser to list its securities on Nasdaq.

NASDAQ Listing Center requires companies to meet at least one of three distinct financial standards. Each standard has different requirements, and companies can choose the standard that best fits their situation.

Note: Listing requirements change periodically. Confirm current standards with NASDAQ and your securities counsel.

Standard 1: The Equity Standard (Most Common for Reg A Issuers) – Typically for Nasdaq Capital Market

The Equity Standard is the most commonly used standard for companies transitioning from Regulation A to NASDAQ listing, particularly for the Nasdaq Capital Market.

Requirements:

For Regulation A issuers, the Equity Standard is often the easiest path because:

A company must have at least 1,000,000 unrestricted publicly held shares and at least 300 round lot holders to list on the Nasdaq Capital Market. The company satisfies these requirements by demonstrating the applicable market value, recent trading price, and average monthly trading volume of its securities.

Standard 2: The Market Value Standard – Typically for Nasdaq Global Market

The Market Value Standard requires higher market capitalization and is often used for listing on the Nasdaq Global Market.

Requirements:

The value of unrestricted publicly held shares and the most recent trading price are key liquidity metrics. The company must demonstrate compliance with these standards, and the company satisfies the minimum market and liquidity requirements for the Global Market.

Standard 3: The Total Assets/Total Revenue Standard – Typically for Nasdaq Global Select Market

The Total Assets/Total Revenue Standard is often used for the Nasdaq Global Select Market, which requires companies to meet all criteria under at least one of four financial requirements and applicable liquidity requirements.

Requirements:

The Nasdaq Global Select Market has the highest standards, and companies must meet the minimum market value, net income, and other financial thresholds. Under the net income standard, NASDAQ proposes to increase the minimum Market Value of Unrestricted Publicly Held Shares (MVUPHS) from $5 million to $15 million.

For all tiers, continued listing requirements and quantitative continued listing requirements must be met, including maintaining the minimum bid price and market value of unrestricted shares. The company's securities must demonstrate sufficient liquidity, as measured by the market value of unrestricted publicly held shares, recent trading price, and average monthly trading volume.

A new NASDAQ rule became operative on April 11, 2025, and significantly changed how smaller companies can satisfy initial listing requirements for IPOs and uplists. This change directly affects companies planning to uplist from Regulation A.

Important: Engage securities counsel to understand how this rule applies to your specific situation.

The Change: Public Float Requirement Strictness

Under the newly approved rule, a company completing an IPO or an uplist from the OTC must meet the applicable Public Float Requirement solely with proceeds from the offering. This means:

What This Means for Regulation A Issuers:

Impact on Your Fundraising Strategy:

This change makes it more difficult for smaller companies to meet listing requirements, but it also ensures that companies listing on NASDAQ have genuine market demand and investor participation.

NASDAQ requires minimum shareholder counts and specific distribution standards. Understanding these requirements helps you plan your Regulation A raise and post-raise shareholder management.

Minimum Shareholder Requirements

What "Round-Lot" Means for Your Regulation A Raise

A "round lot" is typically 100 shares. NASDAQ requires that at least 50% of your shareholders hold shares worth at least $2,500. This means:

For Regulation A issuers, this creates an important strategic consideration. Your minimum investment size should encourage round-lot purchases. Companies that set minimum investments of $2,500-$5,000 naturally create round-lot holders.

Shareholder Distribution Standards

Beyond minimum counts, NASDAQ requires shareholder distribution across:

Your Regulation A raise required PCAOB-audited financial statements. That's your foundation. But NASDAQ listing requires significantly more frequent and rigorous reporting.

Regulation A Reporting Requirements

NASDAQ Reporting Requirements

Timeline Requirement for Operating History

Companies seeking listing in connection with a Regulation A offering must have a minimum operating history of two years at the time of listing approval. This means:

The Audit Transition: From Annual to Quarterly

The transition from annual Regulation A reporting to quarterly NASDAQ reporting requires significant accounting infrastructure:

NASDAQ requires companies to meet high standards of corporate governance. These requirements are more rigorous than Regulation A requirements and must be implemented before listing approval.

Board Structure Requirements

Your board must meet specific composition and independence requirements:

Audit Committee Requirements

The audit committee must consist of at least three independent directors:

Compensation Committee Requirements

The compensation committee must consist of independent directors:

Nominating/Corporate Governance Committee Requirements

The nominating committee must consist of independent directors:

Policies and Codes: Mandatory Documentation

Beyond committee structure, NASDAQ requires:

Your transfer agent must be DTC-eligible and capable of handling electronic book entry shares. This is a critical requirement that many companies overlook.

What DTC Eligibility Means

DTC (Depository Trust Company) is the central securities depository in the United States. All NASDAQ-listed companies must use DTC for settlement and clearing. Your transfer agent must:

Transfer Agent Migration: Planning the Transition

If you've been using a traditional transfer agent for your Regulation A raise, you likely need to upgrade or migrate to a DTC-participating agent. This process includes:

The difference between a successful uplist and a failed one often comes down to operational readiness. You need systems that handle volume, speed, and compliance demands of public markets.

Your Regulation A raise likely brought you 5,000-40,000 shareholders. NASDAQ uplisting can double or triple that number within months. You need infrastructure to manage:

Cap Table Management

Shareholder Onboarding at Scale

Dividend and Distribution Processing

Proxy Voting Administration

Investor Communications Infrastructure

DealMaker's platform handles this natively—your Regulation A investor base can transition directly into post-listing shareholder management without data loss or re-verification.

Once public, you're filing with the SEC's EDGAR system on strict deadlines. Missing a filing deadline can trigger delisting proceedings.

Form 8-K: Current Event Filings

Form 10-Q: Quarterly Financial Reports

Form 10-K: Annual Financial Reports

Regulation FD Compliance

You need automated systems for:

Your Regulation A raise required KYC verification of every investor. That work doesn't disappear after uplisting—it intensifies.

You need documented:

Regulatory Audit Expectations

Regulators audit KYC/AML compliance regularly. You need to demonstrate:

Your Regulation A raise likely involved multiple payment methods (ACH transfers, wire payments, credit cards). Uplisting means managing ongoing distributions at scale.

You need:

Post-uplisting, institutional investors demand constant access to information. Your investor relations infrastructure needs.

Investor Portal

FAQ Management

Event Calendar Management

Quarterly Update Distribution

The 12 months before your NASDAQ application should focus on operational cleanup and preparation:

Share Structure Optimization

Shareholder Communication Strategy

Market Maker Cultivation and Commitment

Financial Audit Preparation

Your Regulation A story was community-driven: "Join us. Be part of our mission." Your NASDAQ story is institutional: "Here's our market opportunity, competitive advantages, and path to profitability."

Institutions care about:

Reframe your Regulation A case studies and customer wins as proof of market validation, not just community support.

NASDAQ requires minimum trading volume and spread stability. Work with your market makers on:

Time your announcements strategically:

Your Regulation A investors are your foundation. Don't lose them post-uplisting. Instead:

Before you file your NASDAQ application, measure:

Your first quarter as a public company sets the tone. Monitor:

Institutional adoption follows analyst coverage. Track:

Your Regulation A investors are your retention test. Measure:

Public companies live or die by operational excellence:

Note: Past performance does not guarantee similar results. Each company's circumstances and outcomes were unique.

Newsmax: Regulation A+ to NYSE Listing

Newsmax completed a Regulation A+ offering through DealMaker, raising the maximum $75 million and listing on the New York Stock Exchange (ticker: NMAX) on March 31, 2025. The company built a substantial retail shareholder base during its capital raise before transitioning to major exchange listing.

Key metrics:

What this demonstrates: Regulation A successfully builds the operational infrastructure and shareholder base needed for major exchange listing.

Disclaimer: Timelines and metrics described are based on historical examples and may vary significantly. Engage professional advisors for guidance specific to your situation.

Q: How long does the entire process from Reg A to NASDAQ listing take?

A: The typical timeline is 18-24 months from Regulation A qualification to NASDAQ listing. This includes 6 months for Regulation A qualification and raise, 6 months for operational preparation, 6 months for NASDAQ application review, and 6 months for final approval and listing preparation.

Q: Can I list on NASDAQ immediately after completing my Regulation A raise?

A: No. Companies seeking listing in connection with a Regulation A offering must have a minimum operating history of two years at the time of listing approval. This two-year requirement ensures companies have demonstrated sustained operations and financial stability.

Q: What are the minimum financial requirements for NASDAQ listing?

A: NASDAQ has three financial standards. The Equity Standard (most common for Reg A issuers) requires $10 million in stockholders’ equity and $5 million in market value of unrestricted publicly held shares. The Market Value Standard requires $50 million in market value of listed securities. The Total Assets/Total Revenue Standard requires $50 million in total assets and $50 million in total revenue.

Q: How many shareholders do I need for NASDAQ listing?

A: You need a minimum of 400 shareholders (or 300 if average daily volume exceeds 2,000 shares). Additionally, at least 50% of your shareholders must hold shares worth $2,500 or more (round-lot holders). For Regulation A issuers, this is typically achievable since Reg A raises create thousands of shareholders.

Q: What happens to my Regulation A investors after I list on NASDAQ?

A: Your Regulation A investors become NASDAQ shareholders. Their shares remain valid and tradeable on the NASDAQ exchange. Companies that successfully retain their Regulation A shareholders post-listing see higher average holding periods, lower shareholder churn, and stronger brand loyalty.

Q: Do I need market makers to list on NASDAQ?

A: Yes. NASDAQ requires 3-4 committed market makers before listing approval. Market makers are critical because they provide liquidity, which attracts institutional investors and ensures trading volume on day one of listing.

Q: What is the April 11, 2025 rule change and how does it affect me?

A: The April 11, 2025 rule change requires companies completing an IPO or uplist from OTC to meet the applicable Public Float Requirement solely with proceeds from the offering. This means you cannot count “free trading” shares from prior private placements. Your Regulation A raise must generate sufficient public float on its own.

Q: What is the process for listing on NASDAQ?

A: The process includes preparing your company for public markets, submitting an application, and meeting all listing standards. The primary market is where your securities will be initially listed and traded, establishing the foundation for your public trading activity.

Q: How do private placements affect NASDAQ listing?

A: Private placements can impact your public float and shareholder base. Recent private placement market activity, including valuations and trading, may influence your eligibility and the listing requirements you must meet.

Q: What is involved in transferring a company to NASDAQ?

A: Company transferring from a foreign regulated exchange or another market must meet Nasdaq’s listing standards, including requirements for trading history, market value, and trading liquidity. The process ensures the company is compliant with all applicable rules before listing.

Q: How do acquisitions affect NASDAQ listing standards?

A: If your company is involved in one or more acquisitions, you may be subject to additional listing standards, especially if securities are issued to fund or are associated with those acquisitions.

The regulatory environment is evolving, but the opportunity for companies to transition from Regulation A to NASDAQ listing is real and achievable. Companies that move intentionally—building investor communities through Regulation A, establishing public company discipline, and preparing their infrastructure—can uplist successfully.

The key is treating your Regulation A raise not as an endpoint, but as the beginning of your public market journey.

Final Disclaimer: This is educational material only. Before pursuing any capital raising or listing strategy, engage qualified securities counsel, financial advisors, and compliance professionals. DealMaker makes no representations about the feasibility or suitability of strategies described for your particular situation.

.png)

.jpg)

.png)

.jpg)

.jpg)